Practical budgeting tips and savings strategies for American families juggling healthcare and education expenses

financial planning

Managing family finances effectively in the United States is a critical skill, especially when healthcare and education costs continue to rise. Families nationwide face the challenge of balancing essential expenses while planning for future financial security. This blog will provide a comprehensive, SEO-friendly guide on how to manage family finances with a special focus on the high costs of healthcare and education in the US. Covered topics will include budgeting tips, insurance optimization, education savings plans, and strategies to maximize financial resources—all geared towards readers aiming for better money management and higher eCPM value through relevant keywords.

How to Manage Family Finances with US Healthcare and Education Costs

In the modern US economy, managing family finances can feel overwhelming. Healthcare spending and education costs often represent the two largest financial burdens for families. Rising hospital bills, insurance premiums, medical expenses, tuition fees, and student loans can stretch any budget to its limits. However, with strategic financial planning, it is possible to take control of these costs, reduce stress, and build a stable financial future.

This article aims to guide families step-by-step on how to budget, save, and invest wisely to handle these hefty expenses while maximizing opportunities for tax savings, insurance benefits, and educational financial aid.

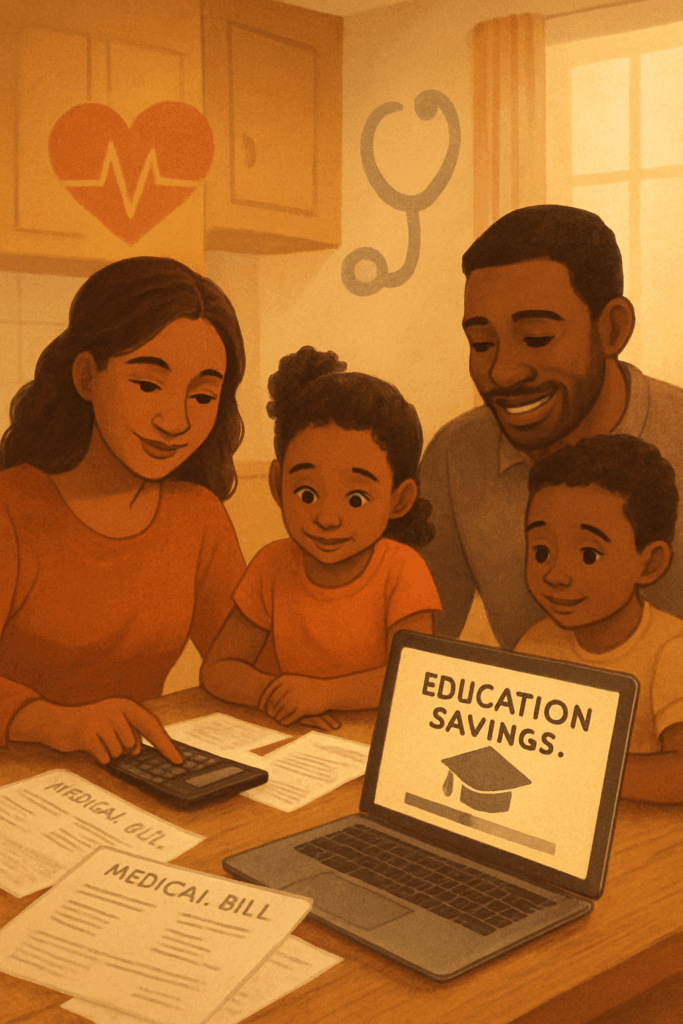

Understanding the Financial Impact of Healthcare in the US

Healthcare costs in the US are notoriously expensive, with many families paying thousands annually in insurance premiums, co-pays, deductibles, and out-of-pocket expenses. According to estimates, the average American family spends about $5,000 to $10,000 each year on healthcare alone. Unexpected medical emergencies only add to this burden, making healthcare one of the top contributors to household financial stress.

Tips to Manage Healthcare Costs

- Choose the Right Health Insurance Plan: Review and compare health insurance plans annually during open enrollment periods. Opt for a plan that balances monthly premiums with deductibles and out-of-pocket maximums tailored to your family’s medical needs.

- Utilize Health Savings Accounts (HSAs): HSAs provide tax advantages for families with high-deductible health plans. Contributions are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are tax-free, creating a triple tax advantage.

- Use Preventive Care and Wellness Programs: Many insurance providers offer free preventive care services which help reduce long-term costs by catching health issues early.

- Shop Around for Medical Services: Costs for procedures and tests can vary widely between providers. Use online tools and insurance resources to compare prices.

- Negotiate Medical Bills: Don’t hesitate to negotiate bills or request payment plans if faced with a large medical expense.

Tackling Education Expenses: Saving for College and Beyond

Education in the US is a significant investment, with average college tuition costs exceeding $25,000 per year at private institutions and even public colleges averaging above $10,000 annually for residents. Student loan debt is a growing concern for millions, making early financial planning essential.

Effective Strategies for Managing Education Costs

- Start a 529 College Savings Plan: 529 plans are tax-advantaged savings accounts designed to help families save for future education costs. Earnings grow tax-deferred and withdrawals for qualified education expenses are federally tax-free.

- Research Scholarships and Grants: Encourage your children to apply for scholarships and grants, which do not require repayment.

- Consider Community Colleges and In-State Schools: Starting at a community college or choosing in-state public universities can significantly reduce tuition bills.

- Explore Employer Tuition Assistance Programs: Many employers offer tuition reimbursement or assistance as part of employee benefits.

- Create an Education Savings Budget: Estimate future education costs and set up automatic monthly contributions toward this goal.

Building a Family Budget That Accommodates Healthcare and Education

Creating a family budget that accounts for these significant expenditures requires discipline and clarity about your household financial situation. Start by tracking all income sources and expenses for a month to identify areas for improvement.

Steps to Create an Effective Budget

- Categorize Expenses: Separate fixed costs (mortgage/rent, insurance premiums) from variable costs (utilities, groceries, medical bills).

- Allocate Specific Funds for Healthcare and Education: Treat these as non-negotiable categories in your budget to prioritize funding.

- Build an Emergency Fund: Aim to save 3-6 months’ worth of expenses to cover unexpected healthcare costs or education-related emergencies.

- Review and Adjust Periodically: Life changes, so should your budget. Conduct quarterly reviews to make sure your budget still fits your family’s circumstances.

Maximize Tax Benefits and Credits for Families

The US government provides several tax incentives to help families manage healthcare and education costs.

- Child and Dependent Care Credit: Helps offset qualified childcare expenses.

- American Opportunity Tax Credit (AOTC): Offers a credit for eligible education expenses during the first four years of college.

- Lifetime Learning Credit: Credits for qualified tuition and related expenses for postsecondary education.

- Medical Expense Deductions: Deduct qualifying unreimbursed medical expenses exceeding 7.5% of adjusted gross income (AGI).

Utilizing these credits and deductions can reduce your overall tax bill and increase available funds for other family needs.

Leveraging Employer Benefits for Healthcare and Education

Many employers offer comprehensive benefits that can alleviate financial pressure.

- Flexible Spending Accounts (FSAs): Allow you to set aside pre-tax dollars for healthcare expenses not covered by insurance.

- Tuition Assistance Programs: To support continuing education or dependents’ education.

- Wellness Programs and Preventive Health Incentives: Often include financial rewards for healthy lifestyle behaviors.

Families should explore all available employer benefits to maximize savings.

Planning for Long-Term Financial Security

While managing immediate costs is crucial, families should also look ahead to long-term financial stability by:

- Investing in Retirement Accounts: Despite other priorities, don’t neglect retirement savings (401(k), IRA) to avoid burdensome financial reliance later.

- Life and Disability Insurance: Protects family income against unforeseen events.

- Estate Planning: Ensure wills, power of attorney, and trusts are in place to safeguard assets for children and dependents.

Conclusion

Managing family finances in the US amid costly healthcare and education demands careful planning, strategic budgeting, and optimal use of financial tools. By choosing the right insurance plans, saving early for education through 529 plans, leveraging tax credits, and utilizing employer benefits, families can reduce financial stress and build a secure future.

This proactive approach not only helps manage day-to-day expenses but also positions families for lasting financial health. For anyone managing a household budget in the US, focusing on these key areas is essential to navigate economic challenges while maximizing income and minimizing liabilities.